Export

Information on export proceduresI. LEGAL BASIS

1. Act Number 17 Year 2006 concerning the Amendment of Act Number 10 Year 1995 concerning Customs.

2. Indonesian Government Regulation Number 55 Year 2008 concerning the Export Duty Imposition on Exported Goods.

3. Regulation of Minister of Finance number No. 145/PMK.04/2007 as amended by Regulation of Minister of Finance number No. 148/PMK.04/2011 as amended by Regulation of Minister of Finance number No. 145/PMK.04/2014 concerning the Provisions of Customs in Exportation.

4. Regulation of Minister of Finance Number 214/PMK.04/2008 as amended by Regulation of Minister of Finance No. 146/PMK.04/2014 as amended by Regulation of Minister of Finance No. 86/PMK.04/2016 concerning Export Duty Imposition.

5. Regulation of Minister of Finance number 224/PMK.04/2015 concerning the Control of Importation or Exportation of Restricted and/or Limited Goods.

6. Regulation of Minister of Finance number 13/PMK.010/2017 concerning the Establishment of Exported Goods Subject to Export Duty and Export Tariff.

7. Regulation of Director General of Directorate General of Customs and Excise Number PER-32/BC/2014 as amended by PER-29/BC/2016 concerning the Procedures of Customs in Exportation.

8. Regulation of Director General of Customs and Excise Number P-41/BC/2008 as amended by PER-18/BC/2012 as amended by PER-34/BC/2016 concerning the Declaration of Export Customs.

II. EXPORT AT A GLANCE

1. Export is an activity of taking out goods out of the customs territory.

2. Exported goods is a goods whose declaration of exported goods has been submitted and has received its application number.

3. Exporter is an individual or legal entity conducting exportation.

4. Export Declaration (PEB) is a customs notification used for declaring goods exportation in the form of written on form or electronic data. The format and content of the declaration of export customs is established in the Regulation of Director General of Customs and Excise.

5. Export Service Memorandum (Nota Pelayanan Ekspor (NPE)) is a memorandum issued by the Document Verificator Officials, Service Computerized System, or Goods Inspector Officials on the declared PEB, in order to protect the inflow of the to-be exported goods to the Customs Area and/or its loading into the carrier.

One of the main functions of Directorate General of Customs and Excise is to protect the citizen, domestic industry and national interests, through the control and/or prevention of entry of imported goods as well as the outflow of exported goods with negative and dangerous impacts which are restricted and/or limited by the provisions/regulation released by related Ministry/Agency.

Based on Article 53 Act Number 17 Year 2006 concerning the Amendment of Act Number 10 Year 1995 concerning Customs, it is mentioned that the provisions of restriction and/or limitation issued by the technical institution, must be reported to the Minister of Finance Attn. Director General of Customs and Excise. On the provisions mentioned above, the Director General of Customs and Excise conduct examination and the Director General of Customs and Excise on behalf of the Minister of Finance determine the list of goods which are restricted or limited to be imported or exported based on the Regulation of Minister of Finance Number 224/PMK.04/2015 concerning Control of Import or Export of Restricted and/or Limited Goods, to be controlled by DGCE afterwards.

On the provisions of restriction and/or limitation whose control is conducted by DGCE, can be monitored through the INSW Portal as a single reference for Import and Export Restriction and Limitation on the website www.insw.go.id.

III. EXPORTED GOODS SUBJECT TO EXPORT DUTY

1. That on Exported Goods can be imposed the Export Duty.

2. Exported Goods subject to Export Duty are listed as follows:

a. Leather and Woods;

b. Cocoa beans;

c. Palm oil, Crude Palm Oil (CPO), and its derivative products;

d. Products of metal mineral processing; and

e. Products of metal mineral with certain criteria.

3. The calculation of Export Duty is as follows:

a. In the case of Export Duty Tariff determined based on the percentage of Export Price (advalorum), Export Duty is calculated as follows: Export Duty Tariff x Number of Goods x Currency

b. In the case of Export Duty Tariff determined specifically, Export Duty is calculated using the formula as follows: Export Duty of each Number of Goods x Number of Goods x Currency.

IV. PROCEDURE OF EXPORT

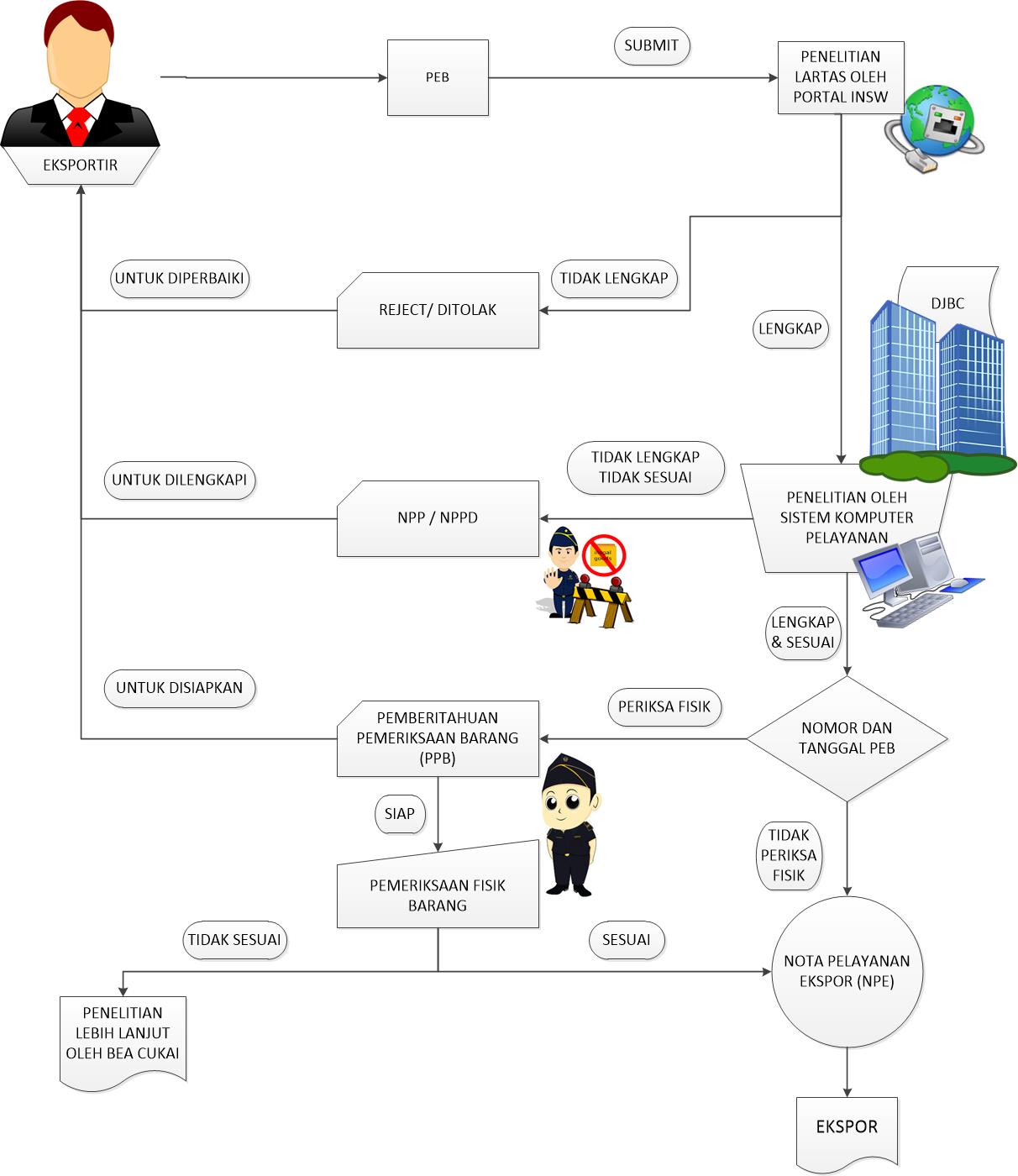

1. Exporter/ its Attorney submit the Export Declaration (PEB) document to the Customs Office of the loading area.

2. On the Export Goods declared in the PEB is conducted the document verification after the declaration document is submitted.

3. If after the document verification the PEB shows that the PEB is not complete and/or different, a response in the form of Rejection Declaration Memorandum (NPP) is released.

4. If in the restriction and/or limitation investigation is shown that the required document has yet to be completed, Required Document Declaration Memorandum (NPPD) is released.

5. If in the verification result of Service Computerized System shows incompletion and difference, as well as not including restricted or limited export goods, or including restricted or limited export goods but their requirement has been fulfilled, as well as goods which do not require physical examination, number and date of submission are written on the PEB and the response in the form of NPE is released.

6. If it is required to do the physical examination, the Goods Examination Declaration (PPB) is released. If the examination of exported goods shows:

a. Results accordingly, Export Service Memorandum (NPE) is released.

b. Results do not fit, to be submitted to the Control Unit to be examined further.

V. FLOW CHART OF CUSTOMS BUSINESS IN THE FIELD OF EXPORTATION

VI. EXPORT PROCEDURE

1. Exporter must declare the to-be exported goods to Customs Office of which good are loaded using PEB (BC 3.0)

2. PEB is made by the Exporter based on the supplementary documents as follows:

a. Invoice;

b. Packing List;

c. Other documents that must be submitted.

3. Exporter must fulfill the provisions of restriction and/or limitation of export imposed by the technical institution.

4. The value calculation of Export Duty is conducted by the Exporter himself by doing Self-Assessment.

5. PEB is reported to the loading Customs Office minimum 7 (seven) days before the expected time of exported goods entry to Customs Area of loading.

6. For the exportation of bulk goods, the exporter of PPJK can submit PEB before the departure of shipping transportation.

7. PEB arrangement can be done by the exporter himself or to be taken care of by the Customs Document Administrator Company (PPJK).

8. To the Customs Office having done the customs PDE system (Electronic Data Exchange), the exporter/PPJK must submit the PEB through the Customs PDE system.

VII. EXPORT GOODS PHYSICAL CHECK

On export goods can be conducted physical check done selectively based on the risk management, which are:

1. Exported goods to be re-exported;

2. Exported goods during which its exportation is purposefully for re-exportation;

3. Exported goods with the exemption facility and/or returning facility;

4. Exported goods with Export Duty;

5. Exported goods which based on the information from the Directorate General of Taxes show that they have the strong indication to cause offence or have done offence against tax laws; or

6. Export goods which are based on the analysis result or information from the Enforcement Unit show the strong indication to cause offence or have done offence against the laws.

Physical examination can be done in:

1. Customs Area;

2. Exporter’s Warehouse; or

3. Other places used by the exporter to keep the Exported goods.

VIII. EXCEPTION OF PEB DECLARATION OBLIGATION

1. Passenger’s personal belongings;

2. Shipping crew’s personal belongings;

3. Border-crossers’ personal belongings;

4. Delivery goods through post under the weight of 100 (a hundred) kilograms.

IX. PENALTY

1. Exporting without submitting the customs declaration is subject to minimum 1 (one) year of imprisonment and maximum 10 (ten) years of imprisonment, as well as to be fined minimum of Rp. 50.000.000 (fifty million rupiah) and maximum of Rp. 5.000.000.000 (five billion rupiah).

2. Submitting fake or fabricated customs declaration and/or supplementary customs documents is subject to minimum of 2 (two) years of imprisonment and maximum of 8 (eight) years of imprisonment, and/or fined at least a hundred million rupiah and maximum five billion rupiah.

3. Not reporting export cancellation to the Officials of Customs and Excise in the Customs Office of loading or reporting export cancellation but after the time period is subject to administration fee of Rp. 5.000.000 (five million rupiah).

4. Incorrectly reporting the type and/or amount of goods is subject to the administration penalty in the form of fine minimum 100% (a hundred percent) and maximum 1000% (a thousand percent) of charges of the country where the fee is not fully paid.